PEGI is exclusively involved in alternate energy.

Investors should think of this company as a combination of a growth stock and utility.

There is more risk with PEGI than a more standard utility.

Out of 29 diversified utilities, Pattern Energy Group (PEGI) is the 9th smallest, with a market capitalization of $1.74 billion. They have the 3rd highest PE (402.25) and 5th highest forward PE (22.25). They also have the highest dividend yield (9.55%).

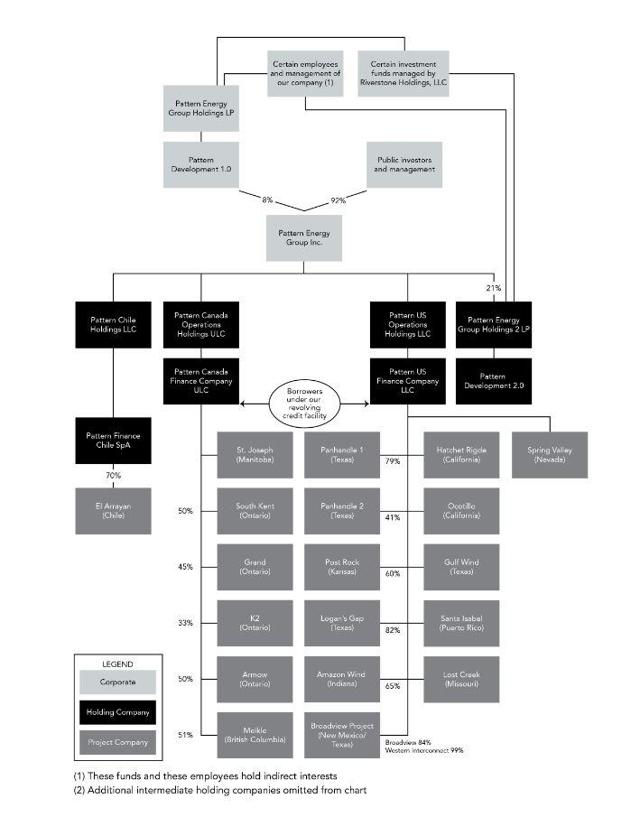

The company has a very complex structure, as shown in this chart from their latest 10K (I'll explain its importance below):

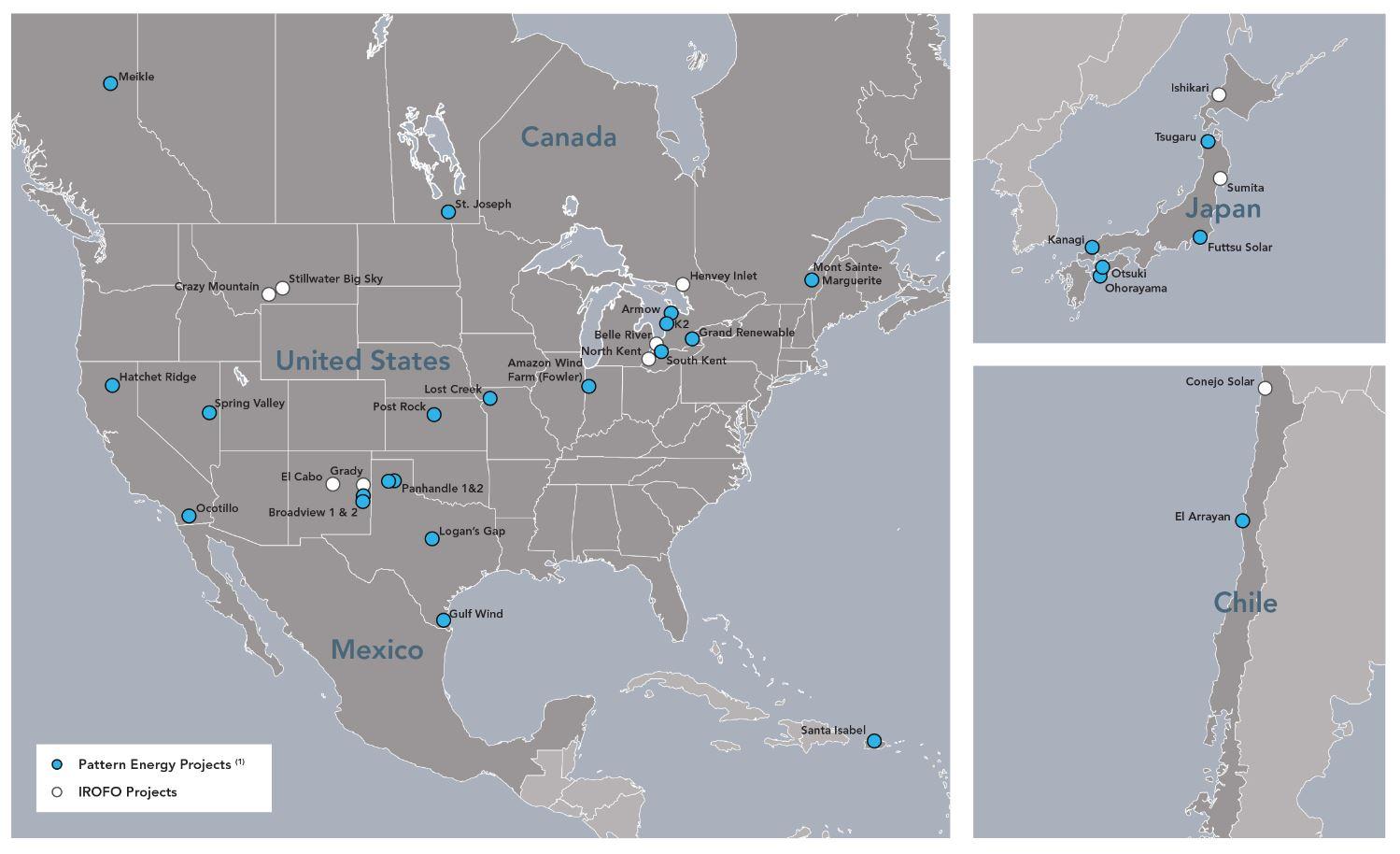

The company is engaged in solar and wind power generation. This map shows the location of all their facilities:

The company is engaged in solar and wind power generation. This map shows the location of all their facilities:

The company owns 25 wind and solar projects that have a little under 3,000 MW of generating capacity. Each project has a long-term contract for "all or a majority of its output." The company has also structured its debt advantageously:

The Company typically finances its wind projects through project entity specific debt secured by each project's assets with no recourse to the Company. Typically, these financing arrangements provide for a construction loan, which upon completion may be converted into a term loan or repaid through capital contributions from the Company and tax equity investors.

Collateral for project level facilities typically include each project's tangible assets and contractual rights and cash on deposit with the depository agents. Each loan agreement contains a broad range of covenants that, subject to certain exceptions, restrict each project's ability to incur debt, grant liens, sell or lease certain assets, transfer equity interests, dissolve, make distributions and change their business. As of December 31, 2017, all projects were in compliance with their financing covenants.

This explains the company's complex corporate structure. What they've done is to (essentially) make each wind or solar project a unique and separate entity. It is financed with its own assets and then establishes long-term contracts. The company pockets the spread between income (supplemented by non-cash charges) and interest payments. Should there be a problem with the contract, creditors will only be able to attach that specific entity, allowing the company's other facilities to remain untouched and out of legal harm's way. This is a very well thought out structure.

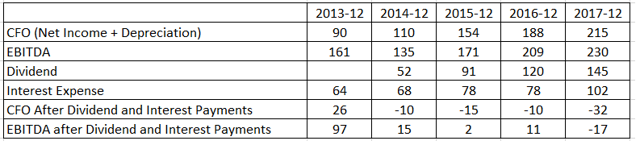

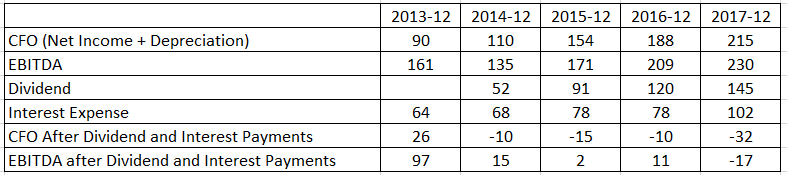

I'm sure that the company's 9%+ yield is attractive. But, it's only natural that dividend investors will see a yield at that level and think, "that can't be safe." As of this writing, there have been no announcements for a dividend cut or an elimination of the dividend. There is a higher probability of that, however. Here is some of the relevant data from their income and cash flow statement (data from Morningstar.com; author's calculations):

{kind=link}

{kind=link}

{kind=link}

The top row shows their cash flow from operations (CFO). I've only added net income and depreciation in order to take a conservative approach (this is actually from one of the older Graham and Dodd Securities Analysis books). I've also included EBITDA from Morningstar's calculations. I've subtracted interest and dividend payments from each; the results are in the bottom two rows. The total after subtracting from CFO is barely negative, which means the company can finance the difference from existing cash, additional debt issuance or one of their credit facilities. The total after subtracting from the EBITDA is just barely positive, save for last year's numbers. Either way, the margin for error is thin. That means that investors should understand the possibility of a dividend cut or suspension is higher than with other utilities. The company acknowledges this point in their latest 10-K under risk factors:

While we believe that we will have sufficient available cash to enable us to pay the aggregate dividend on our Class A shares for the year ending December 31, 2018, we may be unable to pay the quarterly dividend or any amount on our Class A shares during these periods or any subsequent period. Holders of our Class A shares have no contractual or other legal right to receive cash dividends from us on a quarterly or other basis and, while we currently intend to at least maintain our current dividend and to grow our business and continue to increase our dividend per Class A share over time, our cash dividend policy is subject to all the risks inherent in our business and may be changed at any time.

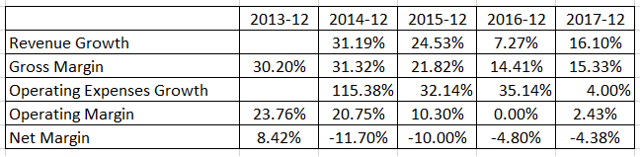

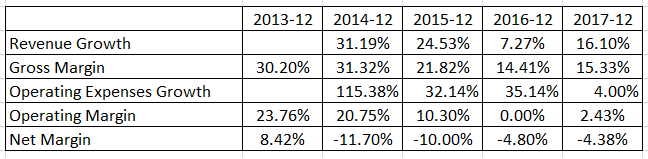

The company, however, is growing at a far faster rate than a traditional utility:

Top line revenue is growing solidly. Their gross margin has dropped to the 14-15% range over the last two years. Operating expenses have increased, which is to be expected as the company has grown. They haven't posted a profit in the last four years, but this company is really more about cash flow than net income at this point.

Top line revenue is growing solidly. Their gross margin has dropped to the 14-15% range over the last two years. Operating expenses have increased, which is to be expected as the company has grown. They haven't posted a profit in the last four years, but this company is really more about cash flow than net income at this point.

{kind=link}

For investors willing to accept this risk, PEGI offers them a well-structured way to become involved with the alternate energy market. However, they should also realize this utility acts as much as a growth stock as a "widows and orphans" investment.

No comments:

Post a Comment